It’s a +2°C world

Code reds and closing windows?

It must be another IPCC report.

Published Monday, the Synthesis Report is a SparkNotes for the prior six IPCC pieces of research (2018-22), themselves the distillation of thousands of climate studies aggregated by hundreds of scientists and signed off by 195 governments.

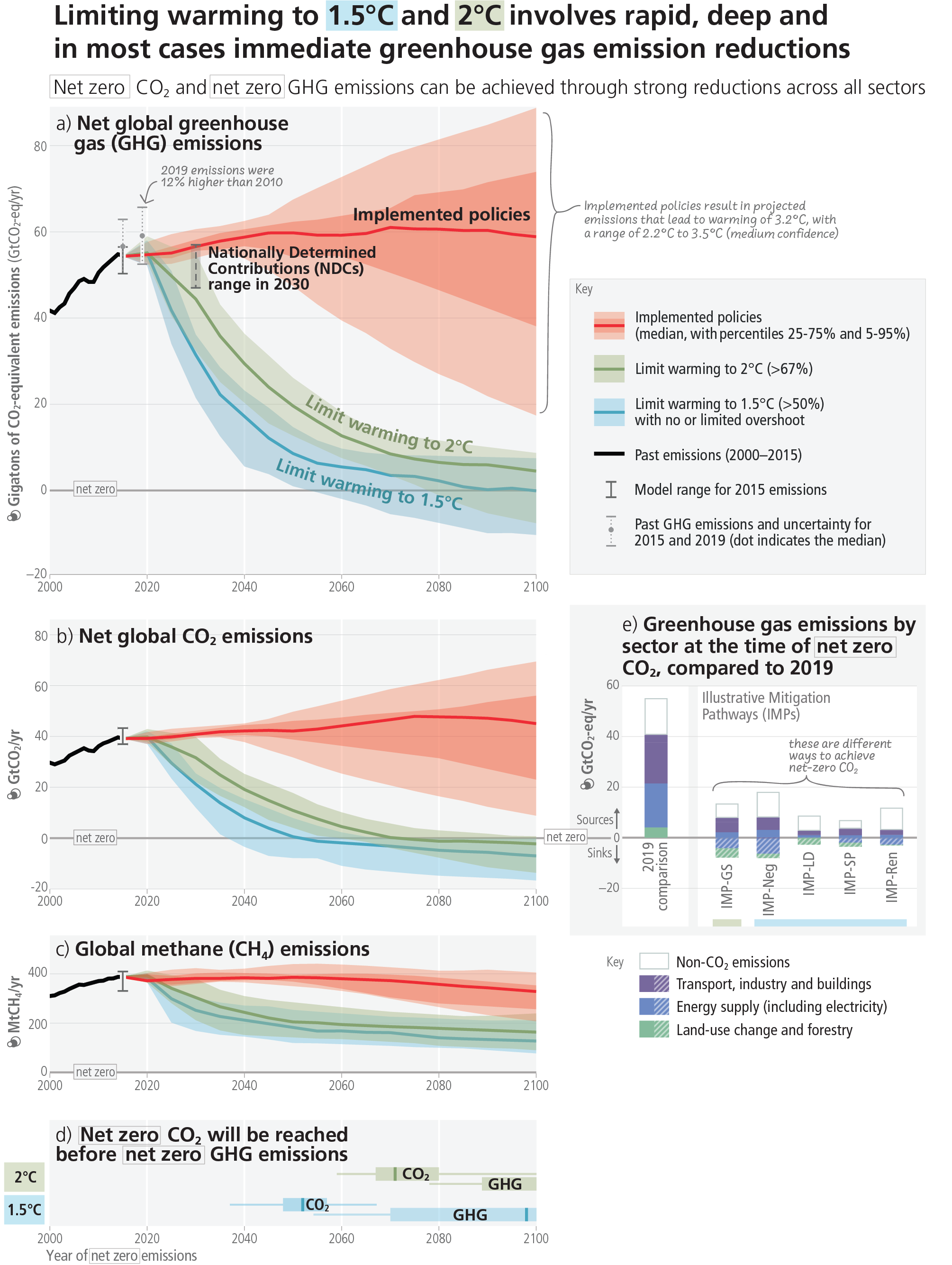

There’s no new science here. This is the final “final warning” we’re going to get for seven years. It’s “now or never” to keep temperatures to 1.5°C above pre-industrial levels. Without “rapid, deep, immediate” cuts, the carbon budget will be depleted by the time the next IPCC review rolls around in 2030.

Spoiler alert...

It’s a safe assumption.

1.5°C is dead in the water. Nobody wants to acknowledge it out loud, for reasons emotional (depressing, defeatist), rational (“1.5°C at any cost” is a powerful political lever), and cynical (developed economies would face more pressure to cough up reparative ‘loss and damage’ and adaptation funds; polluters and policymakers, to make deep cuts). But acknowledge it we must.

The world is up 1.3°C already. The IPCC recognises that overshooting 1.5°C is all but inevitable. Surveyed by Nature anonymously, 60% of IPCC scientists predicted warming of at least 3°C by 2100. Less than six months ago, scientists started calling time on the 1.5°C ‘hopium’ and the UN Environmental Programme (UNEP) conceded there’s “no credible pathway to 1.5°C in place.”

Assuming all policies are met, the IPCC puts us on track for 2.2-3.5°C in this century (see also: Climate Action Tracker, UNEP).

{kind=link}

2-3°C is progress.

We’ll always have Paris (to thank).

In 2016, scientific consensus was flirting with an apocalyptic 4-5°C under a BAU scenario. Halving that figure owes much to the totemic 1.5°C target, which galvanised the public and private action needed to mobilise the energy transition.

Thanks to tanking prices (2010-19: solar -80%; wind -50%), the world is on track to build as much renewable capacity in the next four years as in the last two decades. In its latest World Energy Outlook, the IEA revised to 2025 its projection for peak energy emissions.

Catalysts include the US Inflation Reduction Act (IRA), which should slash US emissions by 40% by 2030 and spur a global clean-energy arms race. Hot on its heels is the EU, with a Green Deal Industrial Plan that augments its emissions reduction package and complements a first-of-its-kind carbon tariff in CBAM. Major policy action is also underway in Japan, South Korea, China, and India.

The world dodged 4°C.

It won’t stay close to 1.5°C.

There exists no 1.5°C scenario where emissions peak after 2024. Countries would need to spend 3-6x more on renewables annually. That would have to be matched by vast efficiency gains and new technologies for transport, industry, and buildings, which are nowhere near on track. Plus, the oil & gas industry would need to slice the 40% of global methane emissions for which it bears (though, even in a year of record profits, refuses to take) responsibility.

In the absence of all of the above, and/or carbon-reduction technologies that barely exist, the IPCC puts forward one last edge of the wedge that could keep the window from closing: Cancel fossil fuels, effective immediately.

Economist: “Our 50/50 shot at meeting 1.5°C was just about credible in 2016. Seven intervening years of rising emissions mean such pathways are now firmly in the realm of the incredible. The collapse of civilisation might bring it about; so might a comet strike or some other highly unlikely and horrific natural perturbation. Emissions-reduction policies will not, however bravely intended.”

Technically possible? Sure.

Politically and economically? No chance.

The world’s two biggest polluters — China and the US — are ploughing ahead with permits. Per recent earnings calls, oil companies are rolling back from renewables and rolling out the carbon bombs. In 2022, it emerged the emissions of all planned fossil fuel projects amounts to 646 GtCO2, i.e. beyond the upper limit of prior IPCC estimates.

Combined with total existing projects, those numbers sling us past the 1.5°C carbon budget of 400 GtCO2, past the 2°C carbon budget of 1,150 GtCO2, and towards an uncertain but balmy future in which land and ocean carbon sinks get a lot less effective at sucking carbon out of the atmosphere.

There’s a mistake in thinking 1.5°C is safe and anything above 2°C is game over. Courtesy of the IPCC, however, we can expect three outcomes:

Even modest increases are going to be disruptive; and

No region in the world will escape disruptions; but

Disruptions will be unpredictable, their impacts variable.

New York Times: “For decades, visions of possible climate futures have been anchored by, on the one hand, Pollyanna-like faith that normality would endure, and on the other, millenarian intuitions of an ecological end of days. Neither looks likely now, with the most terrifying predictions made improbable by decarbonization and the most hopeful ones practically foreclosed by tragic delay. The window of possible climate futures is narrowing, and as a result, we are getting a clearer sense of what’s to come: a new world, full of disruption.”

Investors need to get with it.

Mitigation isn’t enough.

To date and broadly speaking, private flows have been aimed at mitigation over adaptation. Investors have approached climate change as an operational risk to be overcome, either through risk avoidance or sector allocation.

That strategy made sense when there was a shot at 1.5°C. The speculative benefits of an investment thesis predicated on a doomsday scenario is, perhaps, not worth the bad publicity (how do you sell a fund like that?).

It’s not, however, a strategy that makes sense when we’re hurtling towards 2-3°C.

If the following chart is our new reality; if, in the next 50 years, we can expect to see commensurate second-degree effects on productivity and on clean-energy infrastructure that is, ironically, more vulnerable to extreme weather events; then I’m not convinced a clean-energy ETF or ESG integration really cuts it anymore.

Climate is a macro risk. Let’s start treating it like one. (Bear with for part two.)