Nobody wants to invest in climate change

If you haven’t already, I recommend first reading Part 1: It’s a +2°C world.

Paris is dead.

A couple of weeks ago, I said overshooting 1.5°C is a foregone conclusion. TLDR: The incredible pace of decarbonisation steered us clear of an apocalyptic 4-5°C, but it came too late for 2°C and below. Technically possible? Sure. Politically and economically? No chance. The world would need to cancel fossil fuels and summon barely-existent carbon reduction technology. It would need to do so this year.

Company management, asset management, PR companies: I beg of you, rein in the inane 1.5°C Earth-Month bullshit. There is no ‘climate crossroads’, except in the rearview mirror. Suggesting otherwise is worse than intellectual dishonesty or delusion. You don’t need to justify expanding or buying or representing fossil fuels — were I blessed with the prescience of Warren Buffett, I’d have gone all in on Occidental Petroleum as recently as last month, too! — but your hypocrisy is gross.

It’s why we’re in this situation, and it’s what will make it worse yet.

You know, I know, anyone who’s engaged with the science knows we’ll hit 2.5-3.5°C by 2100. In the interest of honesty and absence of evidence to the contrary, it’s safe to assume a middling 3°C (as did 60% of IPCC scientists, when asked anonymously).

Skip the performative obituary. Onwards!

Prepare for a world in 3D.

The recent IPCC Synthesis Report confirms that even modest increases will be more disruptive than previously thought; that nowhere in the world will be immune; and that hazards will be deeply unpredictable, their impact, variable. Since disruption grows exponentially for every degree of a degree, you can go ahead and bold, underline, and italicise all of the above.

For financial systems, there’s an inevitable butterfly effect here:

Primary hazards (drought, heatwaves, floods, fires, biodiversity loss) create

secondary disruptions for local resources (health, food, freshwater, energy, infrastructure (figure below, IPCC)), creating

tertiary consequences for local productivity, creating

quaternary reverberations over global value chains, across which travel 70% of the $28.5T in +6,000 goods/services traded each year, creating

📉 negative economic outcomes for some industries/regions, and

📈 positive economic outcomes for others.

The dark irony of decarbonisation delay is that electricity demand and supply are growing more weather dependent just as weather grows less reliable. That means that Stage 2 (secondary disruptions) is a more sensitive link in the chain than traditional economic models would suggest, making financial reverberations more material than investors might expect.

Everything we know points to the fact that climate change is systemic change. Dear reader, systemic change is not the eventuality for which market participants are preparing.

Deny, deny, deny.

Google “invest in climate change.” You’ll find plenty about preventative measures and crickets for investable outcomes.

Puzzlingly, the vast majority of investment firms continue to approach climate change via traditional operating risk models. Most have two weapons in their arsenal, both primed for mitigation over adaptation. The equivalent of water pistols at a gun fight, neither captures the full suite of risks — let alone opportunities — yielded by 3°C.

European Central Bank, The Macroprudential Challenge of Climate Change: “[There exist] analytical gaps relevant for systemic risk, notably in terms of scope (interaction with financial vulnerability and economic feedback), scale (interconnectedness and contagion between sectors), and horizon (how long-dated shocks could translate into short-term financial stress, alongside a more in-depth modelling of dynamic behaviours).”

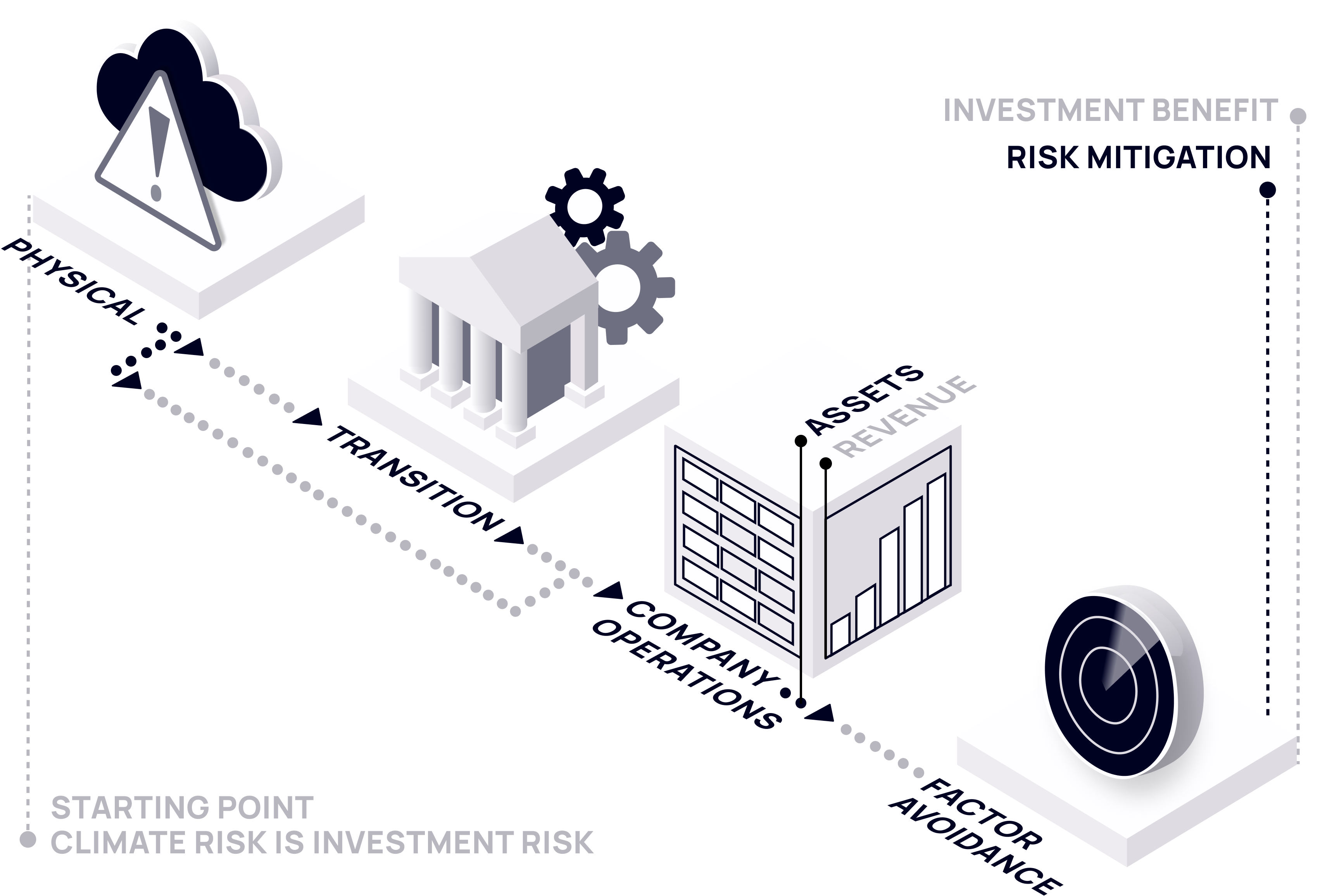

1. Avoid climate risks (outside-in)

Premise: Physical risks are a threat to company profits and portfolio performance, as are the transition risks associated with negative policy and client preference. For companies and shareholders, the objective is to avert potential losses to asset and or portfolio value, respectively.

Drawbacks include:

Limited scope. It’s a useful indicator of downside risk — if, that is, you care only about the immediate business type. For company management, that might be enough. For a bank portfolio or pension mandate? Nope.

Zero alpha. Though it may yield some residual reputational benefit when packaged into a portfolio, any alpha

attributed tomarketed by this strategy is owed, in all likelihood, to quality factor exposure.

2. Mitigate climate risks (inside-out)

(NB: Here I am not referring to private-market/VC (direct) investment in climate tech et al, which does, IMO, present the opportunity for major positive impact and outsized returns.)

Premise: Physical and transition risks are a threat to the environment. The full weight of positive policy and consumer preference will be thrown at decarbonisation. For investors, the objective is to identify companies or sectors that ‘do good’ and, by extension, stand to benefit from transition tailwinds.

Drawbacks include:

Speculative returns. Putting aside the question of whether you can change the world with securities on a secondaries market, ‘do well is doing good’ is the basis for a Disney film, not an investment strategy.

Portfolio risks. The universe of companies or sectors actively ‘doing good’ is pretty small and highly correlated. The appetite for ‘do well by doing good’, on the other hand, is pretty big. Cue some serious concentration and liquidity risks.

So, what gives?

Perhaps the investment complex has genuine faith in 1.5°C. Perhaps acknowledging (and actively preparing for) 3°C is an asset-owner anathema. I suspect a bit of both, compounded by a fatal framing bias embedded in market-cap weighted benchmarking, namely: If present conditions are the baseline against which future returns should be anchored, change will be incremental and linear.

There is another explanation for investor insentience. Investing in change is hard. You don’t have to look further than thematic returns for evidence of that, and climate change is several orders of magnitude more complicated than, say, sustainable urbanised AI EVs for Gen Z (or whatever gimmick it is we’re selling to suckers for 90bps).

To begin addressing climate as a systemic risk, you’d need to understand the impact of weather events on global value chains. That requires models capable of integrating two highly complex (adaptive) systems: meteorology and trade. Citadel may be well on its way, but there isn’t, AFAIK, a single data provider serving the goods.

That doesn’t mean it’s not worth doing. Ask yourself: Had it already materialised, how would I invest in a 3°C world? Take it further: Had it already materialised, how would I invest in a 3°C world in which all of my competitors are convinced it’s still 1.5°C outside?

Not this, not that — then what?

Forget crypto or generative AI. In the 3D economy, the tectonic short-term shocks and long-term shifts provoked by a changing climate will be a macro consideration for every portfolio.

The Big Short ends with a note about the fate of its central characters. Michael Burry, we learn, is now “FOCUSING ALL HIS TRADING ON ONE COMMODITY: WATER.” Retold with reverence, the anecdote summons a Climate-Cassandra Burry who, having found God in SDG 6, turns a discerning eye from CDO swaps to the environmental (and financial!) benefits of water utilities.

As it happens, Burry was not swayed by the water utilities and their environmental (and financial!) benefits, because water utilities are profoundly boring. Instead, he invested in water-rich farmland capable of distributing to water-poor regions, because a world of dwindling freshwater — for which agriculture accounts for a staggering 69% of global consumption — is a considerable risk to the former and opportunity for the latter.

It’s not an isolated example. Just ask any one of the US companies that missed their recent Q3 earnings because a drought in Sichuan, China undercut the hydropower-powered electricity that underpins the manufacturing processes that underpin global supplies of polysilicon and lithium. One of many events, in one of many regions, in one month in 2022.

If Paris is dead, market participants are the frogs stewing in the slow-boiling pot of outdated certainties. The risk here is that one crisis precipitates another; that investors, failing to grasp that 3°C is an inevitability to which they must adapt, miss the pot bubbling over until it’s too late.