Does El Niño cement stagflation?

El Niño has returned to a world economy “flying with one engine.” Unleashed onto vulnerable power, trade, and climate networks, its weather extremes will spark commodity volatility with complex chain reactions. The macro impact may be unusually hard to contain.

Polycrisis? What polycrisis?

It’s official: El Niño is back after four years. The ‘hot phase’ of the world’s most powerful weather fluctuation creates macroeconomic chaos at the best of times. This is not the best of times.

Since 2000, the relationship between El Niño-Southern Oscillation (ENSO) patterns and commodity prices has grown steadily. Non-fuel commodity prices climb 5.3% in the average year after El Niño, as mean global crop yields fall 1.32%, 1.33%, and 0.37% for wheat, rice, and maize, respectively. Metal prices spike when rain-induced floods infiltrate copper mines in Chile or zinc mines in Peru, and drought in Indonesia arrests the hydropower on which nickel mines depend.

Even more pronounced are the reverberations across energy markets, where fuel commodity prices rise by 13.87% in the succeeding year. During drought, power grids buckle under the twin pressures of a) soaring agricultural demand for irrigation (which is energy- and water-intensive, accounting for over 70% of global water consumption), and b) plunging electricity output by hydroelectric and thermal power plants (which are temperature- and water-dependent). Inevitably, countries pivot to coal and crude oil.

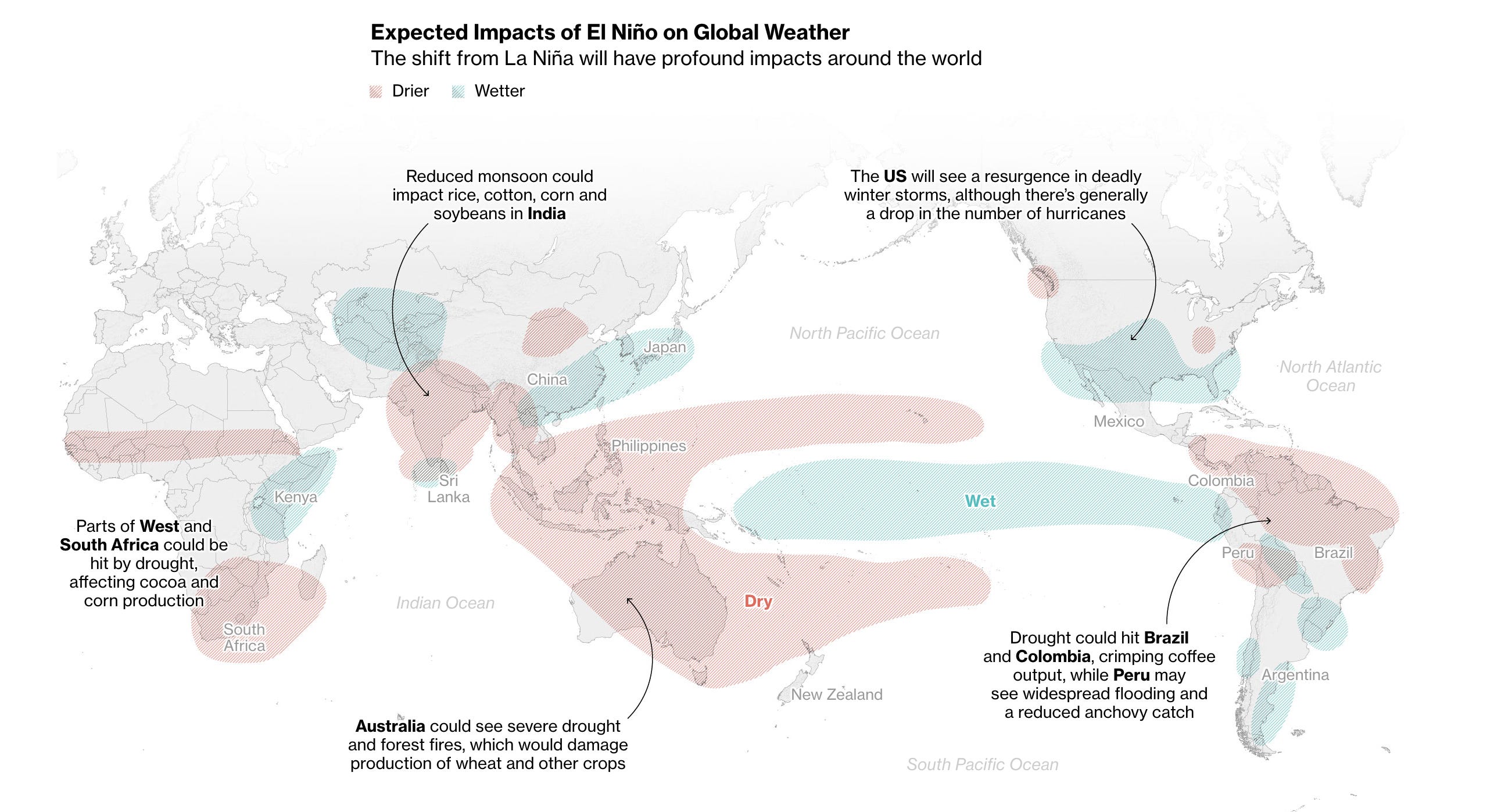

Meteorologists and economists are skilled at anticipating (the effects of) anomalous weather on a regional basis. We know, for instance, that an El Niño beginning on 8 June 2023 results in something resembling the Bloomberg map above. Because the world economy is a complex system, however, neither crude national production nor historical global price data can spell out what lies ahead. There are — always — other idiosyncratic forces at play. Judging by those now dovetailing, this ENSO will have a ✨dramatic✨ fallout.

Hot world. Cool tech. Cold war.

In its official announcement, the US National Weather Service put odds on 56% for a strong and 84% for a stronger-than-average El Niño. Chronic global warming will exaggerate its effects, adding stress to local economies already grappling with climate change (e.g. in South Asia). As El Niño unfurls between now and 2024, expect more clouds and rain in its ‘wet’ regions and more heat and drought in its ‘dry’ regions.

Here’s the kicker: Traditionally, global macro impact is not necessarily a function of ENSO strength. If weather events are synchronised — i.e. simultaneous droughts happen in every region producing commodity X — the price effect is amplified. If asynchronous, the effect is muted. (For e.g.: The US produces extra wheat during El Niño conditions, offsetting depressions elsewhere.)

Against a backdrop of broad (chronic) and deep (acute) weather extremes, ‘offsetters’ have their work cut out. Consider China, recently forced to increase its wheat imports after catastrophic rains (unrelated to ENSO) decimated its harvest — at just the same moment that trading partner Australia, which accounts for 14% of wheat exports, sliced its output forecasts by 34% (barley: 30%) on the back of El Niño.

There’s also the fact that ‘offsetting’ may not work as seamlessly in a brave new world of trade wars and tariff factions; one that happens to be uniquely vulnerable to local weather extremes, given its energy system is increasingly powered by local weather conditions. Which brings us to the two non-meteorological factors to watch. (If not this year, then at the very least in the climate to come).

1. Energy transition

The world has a greater dependency on wind, solar, and hydro energy in 2023 than during the last El Niños of 2019 and 2014-16. Progress? Yes — but renewable energy doesn’t shine when ENSO “changes where the wind is blowing and where the sun is shining.” Generally weaker surface-level wind speeds depress wind output, while a stronger El Niño, one compounded by climate change, is associated with less solar radiation due to increased cloud cover (air moisture content rises 7% per +1°C).

The worse hit local power grids, the more drastic the a) tumble in manufacturing and production and b) leap in fossil-fuel prices. We saw this play out in Sichuan during the comparatively benign climate conditions of August 2022, when drought halved hydropower generation and stymied global supplies of lithium, aluminium and silicon, plus semiconductors, auto parts, solar parts, fertilisers, etc. China turned to coal instead, its booming consumption causing a near-global shortage.

2. Trade tensions

Hot on the heels of COVID-induced hoarding, Russia's invasion of Ukraine sent grain and fertiliser prices rocketing. The Black Sea grain deal and lower gas prices, respectively, brought them back to Earth. Speaking to the FT in January, analysts warned it would take just one of three outcomes — climate anomaly, energy volatility, or deal hostility — to send markets into overdrive again.

“It’s like flying with one engine,” said John Baffes, senior agricultural economist at the World Bank. “As long as that engine works it’s fine, but if the engine stops then you have problems . . . If any of [these risks] materialise, we’ll see a [rise in prices] very, very quickly.” Financial Times

Not to read too much into Russian price floor gambles and grain deal threats, but 3/3 hardly seems a long shot. Given the IMF’s recent warning that 1/3 (namely, a suspended deal) would reduce wheat and corn supplies by 1.5pp and raise global cereal prices by 10%, what the hell does 3/3 look like?

Stagflation!

This environmental-geopolitical nexus will likely usher in a period of commodity and economic disruption, which commodity traders, at least, should have fun with. Perhaps “this is not the best of times,” is the wrong opener. More like “this is the best of times and the worst of times,” depending on where you live, work, and invest.

On a macroeconomic basis, a flurry of commodity price shocks that monetary policy can’t tame sounds more inflationary than Beyoncé. In 2000, the IMF warned a strong El Niño can add 4pp to CPI. One unleashed on a world of stubbornly high inflation and lingering recession risk could increase the risk of stagflation (i.e. stagnation in economic activity + higher inflation) by several orders of magnitude.

Keep an eye on the weather forecast. It might not be the only one, but as a macro factor, climate is rising in rank. The ESNO-induced economic conditions of 2023-24 are a microcosmic preview of what lies ahead.