The water's getting warm

Escalating competition for natural resources blurs the line between environmental and geopolitical risk.

In brief • News to know

🚢 How viable is a trans-Arctic shipping boom? The polar cap is warming 4x faster than the rest of the world, while new NASA research shows Greenland has lost 20% more ice mass than previously thought. Bad news for polar bears probably looks like good news for shipping companies — particularly against a backdrop of crises in the Panama and Suez canals, where transit volumes are down 30% (vs November ‘23) and 37% (vs January ‘23), respectively.

💸 Climate adaptation is gathering pace and attracting dollars. The Northern Sea Route (where transit volumes grew +755% between 2014 and 2022) will be one beneficiary, according to Ray Dalio. Citing climate as one of five growing macro factors, he anticipates “great growth” in adaptation. Urban financing, for a start. A new report, commissioned by the London mayor, has called for a “step change” in climate-resilient infrastructure investment within the capital.

🇨🇳 Beijing got the memo a while back. Its state grid will drop another $70B on infrastructure expansion in 2024, in a bid to keep up with the remarkable pace of renewable development. The International Energy Agency predicts China will create 30% more capacity than the rest of the world between now and 2028, fuelling more demand for rare earth elements. It’s a (growing!) market on which China has an (increasingly tight) 87% grip, cuing more headaches for the US.

In depth • The water’s getting warm

The World Economic Forum (WEF)’s Global Risks Report 2024 is out, and TL;DR: Respondents expect extreme weather to be one of two primary risks in the next two years and the biggest risk in the next decade. Biodiversity loss and ecosystem collapse, natural resource shortages, and (new entrant) critical change to Earth systems are close contenders, in 2nd, 3rd, and 4th place. “Changes emerge silently,” writes the WEF, “but impacts are systemic.”

In short, the most significant dangers in the decade ahead fall into the ‘environmental’ bucket: one of the WEF’s five interwoven categories, which also include geopolitical, societal, economic, and technological risks. But how distinct are those categories, really? How distinct the risks even within one category? Would you glean anything better, or faster, were you to approach two categories (say, geopolitical and environmental risk) through the same lens or a lowest common denominator (say, natural resources)?

It’s still a material world

Narratives around digitalisation / decarbonisation / deglobalisation can obscure a practical economic reality: Competition for natural resources has gone nowhere. Strategic jostling continues to define international relations and economic policy, as it has throughout human history. But it is changing. Escalating, in fact, for four reasons.

More demand, by volume: In 2019, according to Ed Conway, “we mined, dug and blasted more materials from the earth’s surface than the sum total of everything we extracted from the dawn of humanity all the way through to 1950.” The hottest investment themes today are built on the crudest materials. The energy transition has vast unmet material requirements. Thirsty data centres will need a lot more water to keep Chat GPT cool (GPU servers consume 4x more power than CPU).

More demand, by source: Plenty of countries on which the world once depended to extract and export commodities are now consumers, with industries of their own to feed. Cue resource nationalism, as developing economies (Chile, Indonesia, China) seek to contain or secure more value from their exports.

Less supply, by source: Unevenly distributed, commodities — more than any other globally traded good — are uniquely vulnerable to economic fragmentation. Enough to cause mutually assured economic destruction? No, argues Joachim Klement, as “even in an all-out trade war,” commodities would move between power blocs. Still, geoeconomic realities should highlight “the sensitivity of commodity prices to a trade interruption.”

Less supply, by volume: Trade interruptions are inevitable when you have fewer natural resources.

Commodities are in hot water

If there’s one thing climate change and the commodity market have in common, it’s water. Climate change is water risk, and water risk drives commodity markets. Per a (brilliant) recent report by Bloomberg, that makes it a useful indicator for the direction of international trade — and geopolitical risk — in a warming world.

The international exchange of commodities is, in effect, an international exchange of water (to quote Bloomberg quoting Tony Allan, a “virtual water trade”). Physical liquid accounts for just 0.0002% of water traded globally. Since water is a) needed to make, extract, or generate nearly every raw material, and b) unevenly distributed, an organic market — and hidden trade network — has evolved to mitigate resource shortages. “Everywhere there are examples of conflict over water being avoided,” Allan wrote in his first paper on the issue in 1993. “The tendency is to make adjustments which are conflict-avoiding through economic and policy substitutions for water.”

Water availability is climate risk manifest (to steal an overused analogy, “if climate change is a shark, water is its teeth”). The economic risks playing out today are all water-related. Too little of it curtails trade routes, power generation, and crop yields. Too much of it wipes out industrial production. By rewiring water availability, climate change reroutes the invisible trade in water — and so too the visible trade in resources.

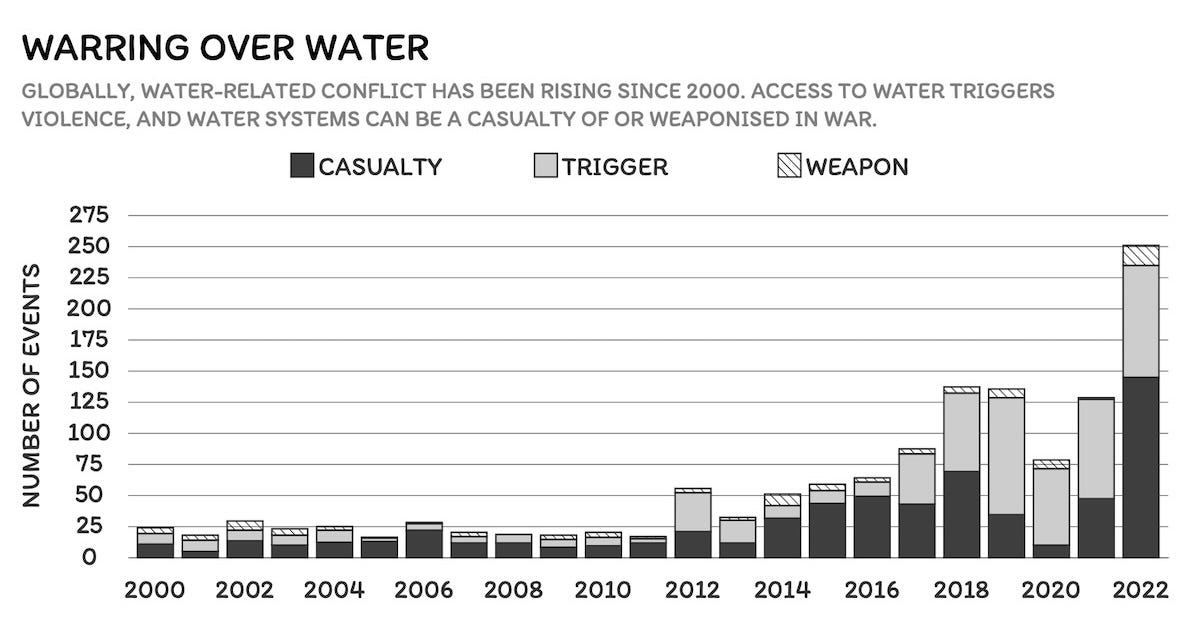

In such a world, environmental and geopolitical risk become even more intertwined and mutually reinforcing. It’s happening already. Per the chart below, water — in addition to and as a proxy for resource constraints — is an increasingly relevant cause and casualty of war.

Water x War is a crude analogy, but you get the idea. Fewer resources (due to climate change) = more competition = fewer resources (due to geopolitical friction) = more competition = fewer resources (due to more geopolitical friction), and so on.

The changing landscape for economic and political risk has unleashed a surge of academic interest in dynamic spillover (see here and here) and a tsunami of words like ‘nexus’ and ‘polycrisis’ and — sigh — ‘black swan’. If you were to take a more straightforward approach to macro analysis in the 21st Century, however, you could do worse than following the flow of water.